Hurricane Harvey made landfall on the south-central coast of Texas one day after the 25th anniversary of Hurricane Andrew’s assault on South Florida. The storm caused massive damage in Rockport, TX. At Category 4, Harvey also ended the country’s longest “drought” of major hurricane landfalls (the last was Wilma in 2005).

While Harvey’s Category 4 winds devastated towns in the immediate landfall area, the focus quickly shifted to the unprecedented flooding in Houston and beyond—ultimately extending for thousands of square miles across southeast Texas.

Harvey Marks the Most Extreme Rainfall Event in U.S. History

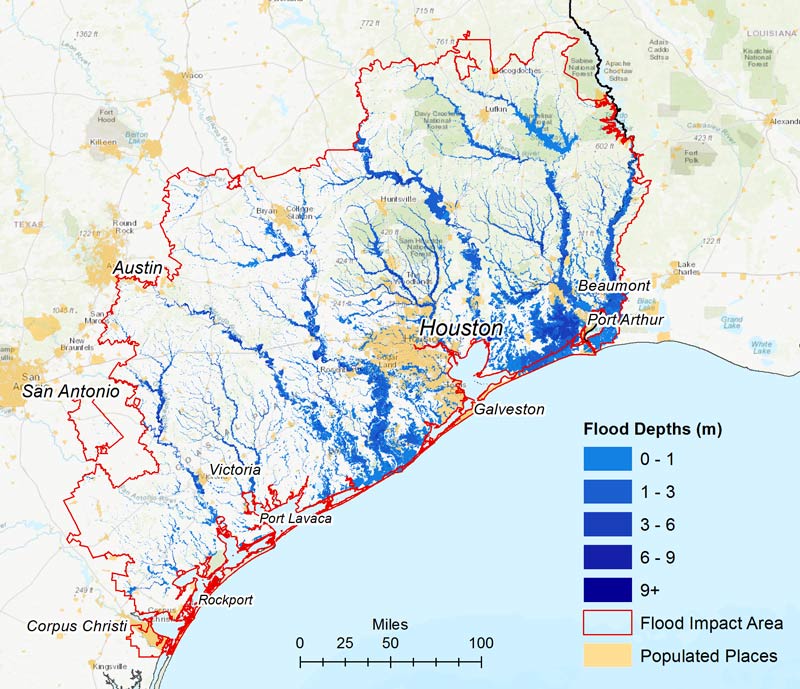

After making landfall near Rockport, TX, on August 25, Hurricane Harvey stalled near the Gulf coast for several days as it dumped prodigious amounts of rain on southeastern Texas and southwestern Louisiana. Harvey broke the record for the most extreme rainfall in the continental United States, with one station just east of Houston registering more than 51 inches of precipitation. All around the city, 30 to 50 inches was the norm.

Harvey submerged thousands of square miles from Rockport, TX, into southwest Louisiana. As the waters recede, the extent of damage to homes and businesses—not to mention infrastructure, farmlands, and the greater ecosystem—is becoming clearer.

How Big Will Harvey’s Losses Be?

Based on simulations of Harvey based on precipitation measurements from the National Weather Service (NWS) and river gauge data from the NWS and the USGS, results from AIR’s U.S. inland flood model indicate that property damage from Harvey’s record-breaking precipitation will be in excess of $65 billion. Total economic losses will be significantly higher.

Perhaps not surprisingly in light of the devastation wrought by Harvey, Harris County ranks first in the country in terms of flood risk (as measured by modeled ground-up average annual loss). AIR estimates that losses to the insurance industry (that is, excluding NFIP payouts) from Harvey will exceed $10 billion, the bulk of which will be driven by flood. The difference between total property damage and the portion that is covered by insurance (even including the NFIP) points to the very large flood “protection gap” that exists in the United States. The availability of a credible catastrophe model—one that captures the risk both on and off the floodplain—provides an avenue for closing that gap, for anticipating possible outcomes, and for fashioning insurance products that are both affordable and profitable.

Flood Resilience of Homes and Businesses

Greater Houston is home to some 6.5 million people. The city’s explosive growth in recent decades has resulted in large expanses of impermeable surfaces—roads and parking lots where absorbent grasslands once were. In Texas, more than 80% of the residential construction is wood. Less than 10% of homes have basements; instead, they are typically built on slab foundations, which are designed to resist flotation or the lateral movement that can result from floodwaters. In Harris County, the elevation of the “finished floor” of new construction must be a minimum of 18” above Base Flood Elevation (BFE). Harris County’s regulations are, in fact, more stringent than the federal standards for communities in Special Flood Hazard areas and apply both to new construction and substantial improvements to existing structures.

More than half of the commercial buildings in the region are steel and concrete and are less vulnerable than residential properties. But their mechanical, electrical, and plumbing systems, if located on the ground floor or in basements, can experience severe damage resulting in high losses.

Harvey and the Flood Insurance Reform Debate

The National Flood Insurance Program (NFIP) was already nearly USD 25 billion in debt when Harvey struck. The program’s current debt limit of $30 billion will surely be reached despite the fact that less than 20% of homeowners affected by Harvey’s flood carry flood insurance, which is only compulsory for homeowners with federally backed mortgages whose homes are located in designated Special Flood Hazard Areas. Under the current authorization due to expire at the end of the month, once the debt limit is reached, the payout of additional claims will need to be explicitly authorized by Congress. What is likely to happen is an emergency reauthorization to cover existing policyholders and then more comprehensive legislation at the end of September.

Even for covered homeowners, payouts are limited by the NFIP’s strict terms and provide no recoveries for living expenses when flooded houses are uninhabitable. Just as after Hurricanes Katrina and Sandy, reform of the beleaguered program is once again in the spotlight, with many roads pointing to increasing the privatization of flood risk as the best viable solution.

Want more information on AIR Flood Solutions?

The AIR Inland Flood Model for the United States

Hurricane Harvey and the Flood Protection Gap

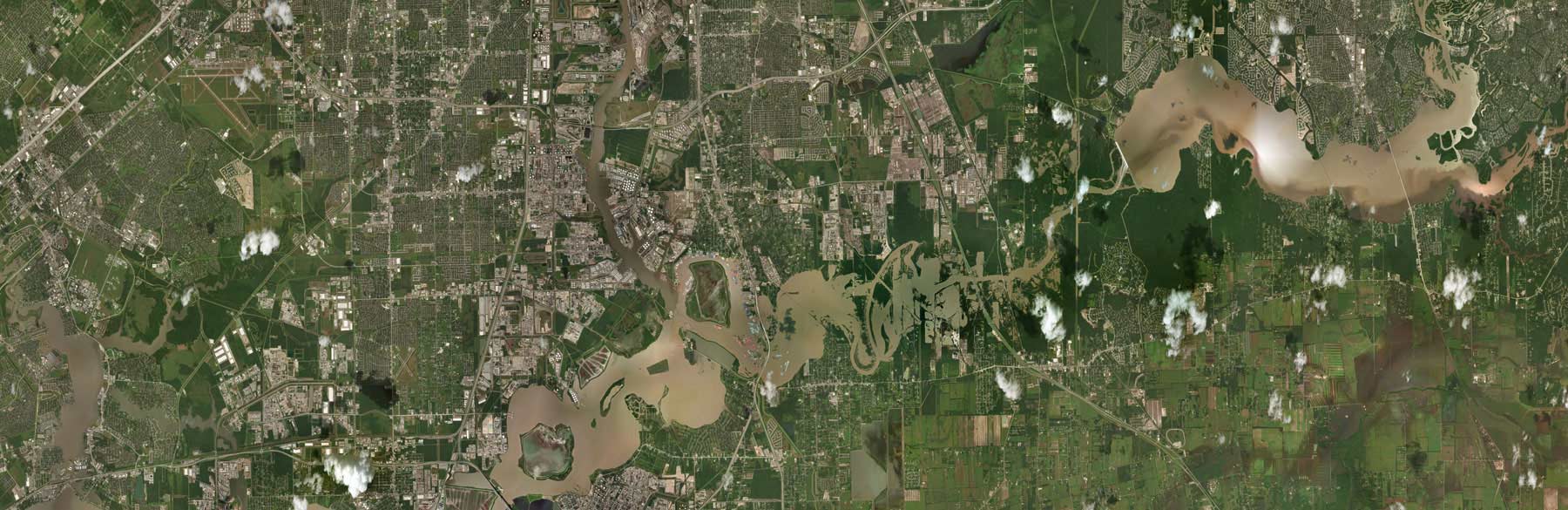

Before and after photo of flooding courtesy of Geomni. ©2017 Geomni. All rights reserved.