Modeling the Extremes: Capturing the Wind Vulnerability of Manufactured and Large, High-Value Homes

Nov 23, 2015

Editor's Note: When it comes to hurricane winds, single-family homes are not a homogeneous class. Design and construction have an enormous influence on how they behave. In this article, we take a look at how structures at opposite ends of the single-family housing spectrum—manufactured homes and large, high-value properties—perform.

The design and construction of single-family residential homes in the U.S. typically receive less engineering oversight than that of commercial and industrial structures. As a result, they experience most of the damage inflicted by hurricane winds. Still, there is a wide spectrum of single-family homes in the U.S., and their design, construction, and location, as well as the presence of secondary risk features, have an enormous influence on how they respond to high winds.

From a hazard perspective, hurricane winds are turbulent, sustained, and change in direction, creating differential pressures on the building envelope from multiple angles. Most damage is inflicted by a complex succession of uplift, suction, and torsional (twisting) forces. When one building element fails, others are at an increased risk. In addition, high winds can hurl debris against structures, causing considerable damage to cladding and windows. Qualitative and quantitative assessment of the vulnerability of differing housing types is crucial for accurate hurricane risk assessment. As with any model, it's always a useful exercise to examine the opposites of the spectrum.

Manufactured Homes

Manufactured homes are factory-built in one or more sections and assembled on-site, with or without a permanent foundation. Most of the interior finishes are installed at the factory and minimal work is done at the site. They are generally less expensive in comparison to modular and single-family homes and sometimes decrease in value over time. Manufactured homes have an integrated chassis, and can theoretically be moved to another location, although in practice few ever are. More than 64,000 units were shipped by manufacturers in 2014, and there are currently more than 8.5 million of them in the U.S. The states with the largest numbers are Florida, Texas, and North Carolina.

Dr. Karthik Ramanathan

Dr. Karthik Ramanathan

Senior Engineer

Dr. Jiazhen Peng

Dr. Jiazhen Peng

Engineer

Edited by Jonathan Kinghorn

The article:

- The wind resistance of manufactured home components, including tie-downs, vary regionally due to variations in construction materials and building regulations.

- Large high-value homes usually feature better quality materials and construction, often incorporate secondary risk mitigation features, and tend to be well-maintained.

- It is important to collect the most detailed exposure data possible when modeling residential property.

Due to their light weight, flat-sided construction, and tenuous foundation connections, manufactured homes are, in general, highly vulnerable to wind damage. Accordingly, the U.S. Department of Housing and Urban Development (HUD) began regulating and governing their design and construction in 1974. Units manufactured before the HUD code was enforced federally in 1976 (still widely known as mobile homes) are the most vulnerable, but as regulations and guidelines have become more stringent, newer units have become progressively more resilient. Year-built information is thus a very important factor in modeling the vulnerability of manufactured homes because it determines the quality of their design, construction, and installation.

Even low to moderate wind speeds can cause significant damage to older manufactured homes, either to the home itself or as a result of failure of the anchorage system. Direct damage often includes blown-off roof panels, loss of roof framing, and loss of wall panels and framing. A manufactured home's cladding can be vulnerable to wind-borne debris, as it may not provide the same level of protection as the monolithically covered wood sheathing common to site-built homes. Windows can be broken as a result of high wind pressure or from the impact of flying debris.

Add-ons such as carports and garages are another major source of damage during hurricanes. Most are not built to the HUD code, and many are not designed to be attached to manufactured homes. Damage to these structures at high wind speeds can cause a breach of the manufactured home's envelope, resulting in significant additional damage to the host structure. Debris from disintegrating add-ons is also a potential source of damage to other homes in the vicinity. This is consistent with the test findings reported by the Insurance Institute for Business and Home Safety (IBHS).

Stronger winds can dislodge manufactured homes from their foundations or blow them over entirely if not properly anchored. Manufactured homes can be anchored using a variety of metal strapping or cable systems. The wind resistance of all components of these homes, including tie-downs, varies regionally due to differing construction materials and building regulations and whether the location is coastal or inland. The age of the home affects its vulnerability as well—even apart from construction codes. All components, including tie-downs, become corroded or worn and therefore more vulnerable over time.

Large, High-Value Homes

Although they present a larger target, large high-value homes are in general less vulnerable to hurricane winds than average-sized single-family homes. They are usually custom-built using better materials and exhibit a high quality of construction, frequently with sophisticated engineering input. They often incorporate secondary risk mitigation features and tend to be well-maintained, all of which adds to their resilience.

Analysis following recent hurricanes shows that, in general, building vulnerability (as characterized by a damage ratio, which is defined as the ratio of the repair cost to the replacement value) decreases as a home's gross area, or square footage increases. Better secondary risk mitigation features, better maintenance, and a lower relative replacement value of different building components are plausible explanations for this inverse relationship. However, a closer look at the vulnerability of buildings to externally applied loads reveals another part of the equation: imposed loads. Post-hurricane damage surveys suggest that a significant driver of insurance claims is damage to roofs from overloading caused by pressure and turbulence or by debris impact.

Differences in building and roof geometry as buildings increase in size mean differences in wind loads. In particular, larger, high-value homes tend to have more complex footprints and roof geometries compared to their average-size counterparts—and that translates to reduced loads.

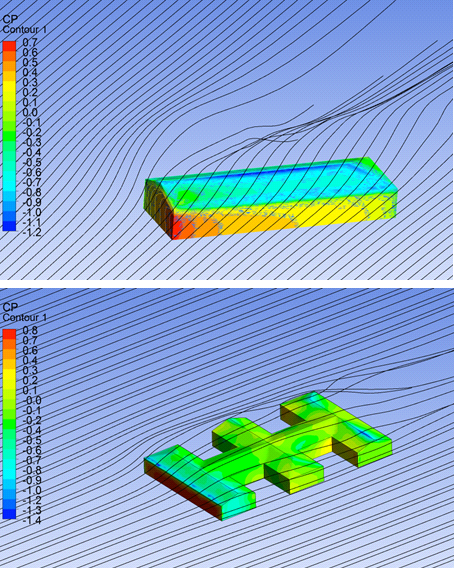

To learn more, AIR engineers conducted experiments using computational fluid dynamics (CFD) to understand the reduction in wind loads with increasing gross area when coupled with increased complexity in roof geometry. Idealized "virtual" buildings representing average and high-value homes were modeled. The added complexity of the larger, high-value homes was captured by changing the number of walls, corners, and the roof type (number of hip and gable ends).

Findings show that as the gross livable area—and consequently complexity of the roof—increases, the fraction of the total roof area subject to damaging critical pressure coefficients decreases. This is because of flow modification due to the structural complexity.

A distinct reduction in vulnerability was noted for homes with a square footage of more than 3,000 square feet. It must be noted, however, that the decrease in vulnerability is asymptotic: Once the square footage is beyond a certain value, there appears to be no further reduction. Note, too, that as wind speeds increase, the mitigative effects of square footage decrease and ultimately disappear.

Conclusion

This article examined single-family homes at opposite ends of the vulnerability spectrum, but homes across the entire range of residential properties exhibit a wide variety of characteristics that affect their vulnerability to hurricane winds. A structure's resilience is determined primarily by its location and design and construction details, but size, age, maintenance history, and other factors also make significant contributions.

Findings from AIR's recent engineering research have been used to inform AIR's U.S. hurricane model update in Touchstone®, which employs wind and storm surge damage functions for different combinations of building occupancy, construction, age, and height classes. These account for the physical response of the structure to a peril, and also quantify the effects of many other macro-level factors including building codes and their enforcement.

For high-value homes, the updated model captures the reduction in vulnerability purely from the standpoint of external pressures or loads. The reduction in vulnerability due to the presence of superior features should be captured by inputting those secondary risk characteristics directly into Touchstone.

While secondary features are not currently supported for manufactured homes in Touchstone, the damage functions have been thoroughly reviewed and updated, and now account for spatial and temporal variation in vulnerability in addition to foundation anchorage systems. In the AIR model, a manufactured home's construction code (which reflects the presence or lack of foundation anchorage), year-built, and location together determine its vulnerability.

It is therefore important to collect the most detailed exposure data possible when modeling residential property, wherever it sits in the spectrum.