Inland Flood Megadisaster in the United States—Are You Prepared?

Jan 29, 2015

Event: A scenario year from the AIR U.S. Inland Flood Model's stochastic catalog

Model: AIR Inland Flood Model for the United States

Stochastic Year ID: 8346

Affected area: Contiguous United States

Estimated ground-up loss: USD 100.8 billion

Annual loss exceedance probability ~1% (100-year return period)

Event Overview

Precipitation-induced inland flood causes more property damage in the United States than any other natural disaster. According to the AIR inland flood model, on average the United States experiences ground-up flood losses of more than USD 25 billion annually, a figure expected to grow with continued development (much in flood-prone areas), rising property values, and increasing numbers of extreme wet-weather events.

This edition of Megadisaster features an entire year of precipitation-induced flood events from the AIR U.S. inland flood model's stochastic catalog. The aggregate ground-up loss—USD 100.8 billion—has an exceedance probability (EP) of about 1% (100-year return period).

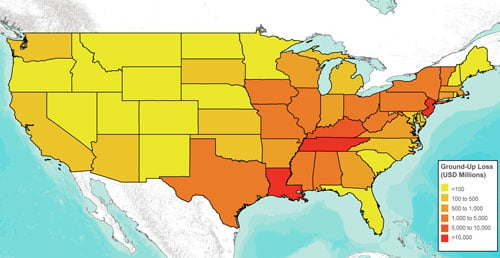

The selected year includes a wide range of events, with on- and off-floodplain flooding in several major river basins, short- and long-duration storm systems, and failed flood defenses. As shown in Figure 1, every state in the contiguous United States plus the District of Columbia experienced inland flood losses during the modeled year. The more costly events during the course of the year occurred in the high-population-density and high-exposure-density eastern and southeastern regions of the country, as they do historically.

U.S. Inland Flood Setting and History

A high-frequency peril, inland floods vary in size, scale, and duration and occur both on floodplains and off. Ranging from localized flooding, waterlogged fields, and briefly blocked roads to widespread inundation and destruction of structures and automobiles, inland flood renders residences uninhabitable and disrupts commercial and industrial businesses.

Although attributed to precipitation (and sometimes exacerbated by snowmelt), the actual storm or storms that caused an inland flood event might not be obvious. Large land areas containing multiple river basins often flood in sequence as rivers are affected by multiple storms occurring over many weeks. Inland flood can be localized or quite widespread, impacting hundreds of counties through a swath of states. In addition, many variables affect the likelihood and intensity of inland flood, including soil type, antecedent soil conditions, drainage conditions, land use and land cover, and flood defenses.

The 3.1 million square mile (8.1 million square kilometer) land mass of the contiguous United States features widely varying types of topography and geology, with millions of miles of rivers and streams (some tidal) and tens of thousands of lakes and reservoirs. The climate also varies widely from sea to sea—from tropical in Florida to dessert-like in the Southwest to quite temperate regions elsewhere, with seasonal rain and snow. Climate has a major impact on flood risk, affecting the amount of precipitation an area receives, the amount of snow on the ground when spring rains begin, and the drying time for buildings and contents.

Approximately 3,800 U.S. municipalities are located on floodplains, while many locales off floodplains also are subject to flood damage and loss. Off-floodplain losses, which typically occur when very intense rainfall causes high levels of surface runoff, are more frequent in urban areas, where the high percentage of paved areas significantly increases the runoff coefficient. Sewer backups and pump failures, insufficient drainage-pipe capacities, and clogged street gutters are common causes of off-floodplain flooding.

Thousands of miles of levees and other flood defenses have been constructed throughout the country (more than 83% of the lower Mississippi River is protected by levees). However, significant flood risk still can exist in areas with a high level of flood mitigation because of the possibility of failure of levees, dams, pumping stations, or other flood defenses.

Catastrophic flood events take place with some regularity, as these recent examples illustrate:

- In the late winter and spring of 2011, heavy precipitation and snowmelt flooded the lower Mississippi River. Advanced flood warnings allowed for intentional levee breaches to prevent flooding in several urban areas, but more than 21,000 homes and over a million acres of agricultural land were still impacted, leaving some areas covered with debris and sediment and contaminated by chemical spills.

- In September 2013, several days of unusually heavy and relentless rain caused highly destructive flash floods in the Boulder, Colorado, region, creating a damaging flow of debris that washed out bridges, homes, and trees.

- Torrential rains from an April 2014 storm system that spawned multiple tornadoes and severe thunderstorms across the Midwest and southeastern United States dumped more than two feet of rain in some areas, resulting in flash flooding across the Florida Panhandle and southern Alabama.

Affected Exposure

The vulnerability of buildings to flood damage depends on many factors, including construction and occupancy, building height, and age. In general, damage due to inundation tends to be nonstructural, affecting interior finishes, such as drywall, plaster, insulation, and flooring, in addition to building content. Basements increase the risk of damage to both contents and the building and contribute significantly to flood vulnerability. In more serious inland flood events, high-velocity flood and debris can compromise the structural integrity of a building, which can lead to the collapse of foundations and the displacement of structural walls.

Damage to residential buildings in the United States is influenced by construction type, elevation of the first floor in the structure, the presence of a basement, and non-engineered components, such as garage doors and main doors. Single-family homes across the country are dominated by wood-frame construction, although masonry is also commonly used. Wood and unreinforced masonry construction typically perform very poorly when exposed to high inundation depths over extended periods.

Unlike residential structures, commercial buildings often are engineered and built to stricter standards, and are thus less vulnerable than single-family homes. Still, mechanical, electrical and plumbing (MEP) systems can experience severe damage, which results in high losses. More than half the commercial buildings in the United States are steel or concrete, which perform better than wood or masonry.

The United States experiences considerable diversity in storm climate. Communities that are most frequently affected by flood generally establish flood-related building regulations and have better flood mitigation practices. Flood-resistant design and construction as specified in building codes, such as International Building Code ASCE 24, complement the National Flood Insurance Program minimum requirements for structures situated in flood-hazard areas. However, construction quality and code enforcement varies widely across the country.

Estimating the Impact

The USD 100.8 billion Megadisaster scenario featured in this article—Year 8346 from the stochastic catalog of the AIR Inland Flood Model for the United States—resulted from 73 distinct flood events of varying size and intensity during the year. Losses occurred in every state in the lower 48 and the District of Columbia and took place in every month of the year.

As shown in Figure 1, state-by-state losses ranged widely. Although losses were concentrated in the Midwestern, mid-Atlantic, and eastern states—reflecting the density of rivers and streams in those areas—California and Arizona also faced high inland flood losses, as did Washington state, in the upper northwest.

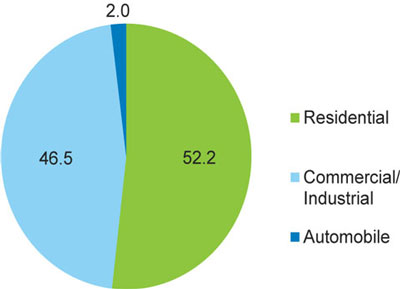

By line of business, residential (including mobile homes) and commercial (including industrial assets) shared in the losses almost equally, as shown in Figure 2.

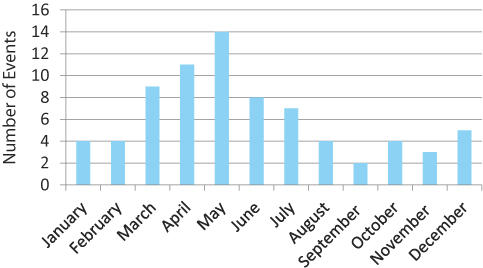

Figure 3 shows the seasonal distribution of the flood events during the year. Inland flood seasonality—which affects the time it takes to dry a building—can have a sizable effect on losses.

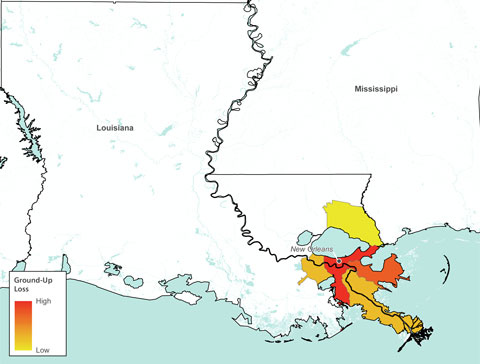

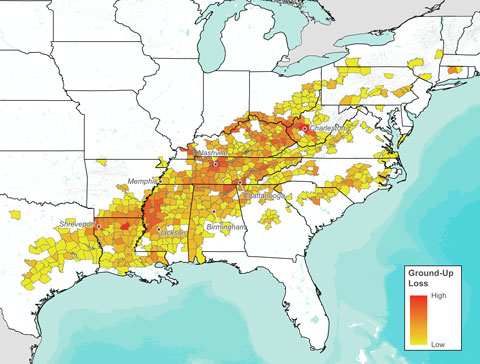

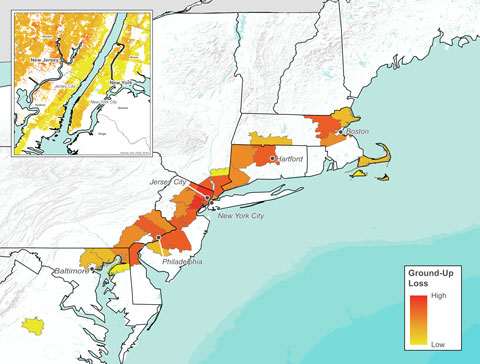

The three most costly events—which accounted for 64.8% of the total ground-up losses for the year—appear in Figures 4, 5, and 6. As shown, these three high-loss events exemplify a variety of inland flood scenarios: a relatively localized flood, a vast event affecting nearly 20 states, and a narrow event along the eastern seaboard that affected a number of major metropolitan areas.

A closer look at the second most costly event (USD 22.4 billion) highlights some of the many complex considerations in assessing inland flood loss potential. A lengthy, seven-day event, the causative precipitation system progressed from northwest Texas through Louisiana, Arkansas, Mississippi, Alabama, Tennessee, Missouri, Georgia, Kentucky, South Carolina, North Carolina, Virginia, Indiana, Ohio, West Virginia, Maryland, Pennsylvania, New York, and Connecticut. Flooding caused damage in more than 600 counties, covering 218,834 square miles (566,777 square kilometers). Impacts included riverine flooding in unprotected areas, failed levees (in Nashville, Tennessee, and Louisville, Kentucky), and off-floodplain flooding from excessive precipitation.

Are You Prepared?

Responsible risk management includes preparing for a wide range of loss scenarios. Using model scenarios to probe your portfolio's strengths and weaknesses will help you respond effectively when disaster does strike.

The various events in this megadisaster loss scenario exemplify the extensive and widespread damage that can result from inland flood. Of course, countless other scenarios could produce equally comprehensive damage, with a similar level of loss. Importantly, the scenario year detailed in this article is not an extreme, tail event. The industry ground-up loss for this inland flood scenario has a modeled annual exceedance probability of about 1.0% (which equates to a 100-year return period); far greater losses are possible.

Being attentive to best practices for an inland flood model can help ensure that you achieve the most realistic loss estimates:

- Strive to obtain highly accurate exposure data. Since inland flood is a highly localized peril, collecting detailed information for the properties in your portfolio—including location, primary building characteristics (such as construction type, occupancy, building age, and height), and a true replacement value—will help refine the loss results and help you get closer to the true vulnerability of the individual buildings.

- Capture secondary risk characteristics. Secondary characteristics for insured property—foundation type, basement levels, basement finish, custom elevation, base flood elevation, first-floor height, custom flood protection, service equipment protection, floor of interest, and contents vulnerability—can have a major impact on modeled losses.

- Understand the flood event definition. Large areas containing multiple river basins often flood in sequence as their rivers are affected by one or more storms. A storm that saturates the ground may or may not be the same storm that causes a river to overflow, making it difficult to isolate the systems causing other flood effects. AIR clusters the extreme runoff and river flows into flood events according to their spatial and temporal proximity, which allows the model to separate the extreme river flows and excess runoff into events that conform to the 168 hours clause.

- Anticipate business interruption losses. You can use the AIR model to calculate business interruption as a function of downtime, damage, building size, and architectural complexity.

- Address the potential for increased losses due to demand surge. Highly concentrated losses can trigger demand surge, an increase in the cost of materials and labor after a large catastrophe due to limited supply. AIR's inland flood model can calculate the additional losses due to demand surge as a function of the total industry loss for each event.

- Be aware of potential losses from non-modeled sources. Modeled losses have been calibrated to and validated against actual reported losses, so the impact of damage due to the force of moving water, debris collision, sedimentation, hazardous material leakage and associated cleanup, and other modeled losses is captured implicitly. Nevertheless, some non-modeled losses can have a sizable impact on losses.

Closing Comments

As the U.S. population grows, so does development in flood-prone areas. With the 2014 release of the AIR Inland Flood Model for the United States, companies can now generate a comprehensive view of precipitation-induced inland flood risk across the geographically and meteorologically complex United States. The model also accommodates the current needs of the industry by incorporating a 168-hour clause when defining a flood event (read this article to learn more).

Catastrophe models are not intended to predict the next megadisaster or when a megadisaster might occur. Catastrophe models do, however, simulate the behavior of physical phenomena and how those phenomena impact the built environment to determine the impact of different perils at a range of intensities in regions throughout the world.

Advanced catastrophe models—thoroughly validated with data from a wide variety of sources—help insurers and reinsurers gain a global perspective on their overall risk. By carefully analyzing model results, risk managers can prepare for a range of contingencies, even megadisasters, such as the multifaceted inland flood scenario presented here.