By now, you’ve heard the phrase “flatten the curve” numerous times to describe slowing the growth of the COVID-19 outbreak. Flattening the curve is critical to avoid overwhelming our healthcare infrastructure (you’ve almost certainly seen stories about shortages of masks, ventilators, hospital beds, and even healthcare employees). In theory, the number of new cases per day may slow down if the right isolation and mitigation measures are taken.

Sounds easy, right? In reality, while there is new data being published and shared regularly, it’s surrounded by a great deal of uncertainty.

Let’s explore why reliable data is so hard to come by, what lessons we can learn from compounding interest in your 401k, or retirement fund, and what might happen when we do flatten the curve.

Where Has All the Good Data Gone?

Publicly available data is rapidly evolving but seems to differ—sometimes significantly—by geography. Why is this the case?

- We’re behind on testing. A shortage of test kits available means we have a backlog of those needing to be tested; even when they are tested and are showing symptoms, in many cases they are being sent home to self-quarantine until test results come in.

- Even when we do test, we are mostly testing those who are symptomatic. To truly understand the transmissibility, severity, and morbidity for COVID-19, we would need the ability to randomly test a significant portion of the population, even those who are asymptomatic. At the current time, most tests are going to those who are showing severe symptoms.

- We may lack the resources for robust contact tracing. Once someone tests positive for COVID-19, those whom they’ve been in contact with for the past 14 days should be tested and have their network traced—we simply don’t have the resources to do this with our current healthcare infrastructure.

- Each data point only represents a snapshot. Data is acquired from various sources and in various formats. Some formats can be automated, but many cannot and may require a person to translate the data into a digestible format.

Many in the epidemiology and public health communities believe the number infected in the U.S. may be up to 10 times what is captured by current testing and reporting—a sobering statistic, especially if mortality rates of ~0.5-4% are accurate. In other countries, underreporting and misreporting are possible, leading to additional uncertainty about what might happen next.

An Analogy for the Quants

Think about flattening the curve a bit like contributing to your 401k or retirement fund. The earlier you start, the more positive benefits you’ll see. Start too late, and even if you contribute more aggressively, it’s possible that you can’t catch up—even increased efforts won’t have the same benefit.

Here is a simple illustration:

| Start contributing at age: |

Annual amount contributed from start year through 65: |

Rate of return: | Balance at age 65: |

|---|---|---|---|

| 20 | USD 5,000 | 7% | ~USD 1.4 million |

| 45 | USD 10,000 | 7% | ~USD 410 thousand |

In a similar vein, the “older” or more advanced an outbreak is, even if our effort to control it or “contribution” is higher, these efforts will be less impactful on the end result. The way in which the outbreak has devastated Italy has displayed just how dangerous it can be to delay social isolation measures.

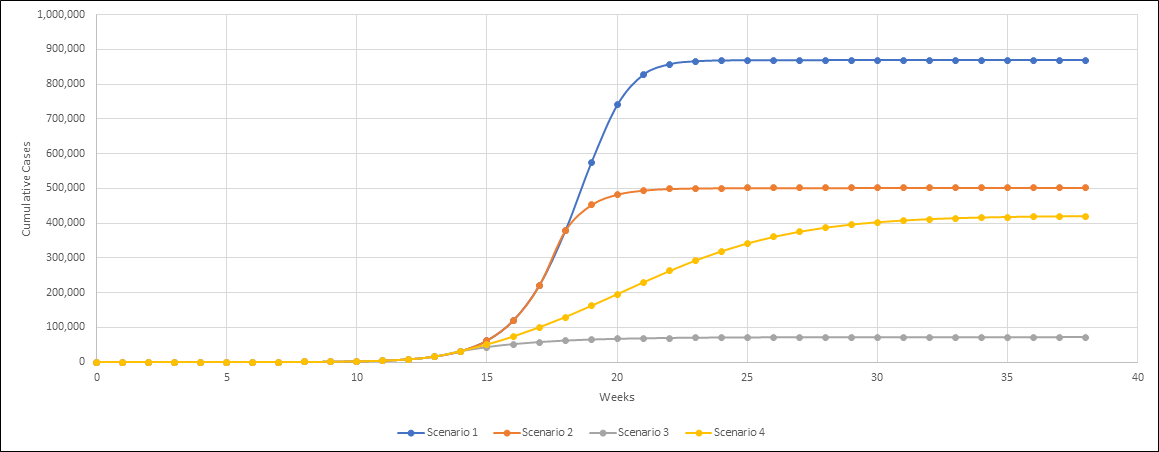

Based on sample data and using methodology from the AIR Pandemic Model, the day on which isolation and mitigation are implemented, and their overall effectiveness in stopping the transmission of the disease, can drive significantly different outcomes (Figure 1):

In the scenarios in Figure 1 the starting R0 (transmission rate) is 2.0, meaning that every person who is infected will then transmit the virus to 2 additional people.

- Scenario 1—No mitigation applied, the only thing that stopped the outbreak was the saturation of infected

- Scenario 2—Mitigation starts in the 19th week and the Rc value = 0.75

- Scenario 3—Mitigation starts in the 15th week and the Rc value = 0.75

- Scenario 4—Mitigation starts in the 15th week and the Rc value = 1.25

If we can get the Rc (transmission rate after active containment) to <1, the virus will die out over time—just look at the significant differences in scenarios 3 and 4, with an identical mitigation start date but a less effective spread after containment.

Similar to our retirement account example above, and to stress the importance of implementing early mitigation efforts, consider scenarios 2 and 4. In scenario 2, mitigation starts just four weeks later, is more effective (Rc <1), and yet it still results in about 80,000 more cases.

Flatten the Curve, and We Can Go Back to Normal—Right?

At some point, the number of new daily cases will slow, and eventually will stop—what happens then?

Serologic testing—which are blood tests to see if an individual is producing antibodies—will be extremely useful to understand the extent of the spread of the virus, what portion of cases are asymptomatic, and perhaps most importantly in the near term, who is protected and therefore unable to catch the virus or spread it to others. In theory, these serologic tests would help us better understand who can return to everyday behaviors without spreading the disease to others and will also be a useful test for which healthcare workers can treat our most vulnerable citizens.

As isolation measures are loosened, we will likely see some resurgence of the disease. It may be difficult to trace, as isolation measures have not been uniform, but our healthcare system and supply chains will have recovered, to some degree. In places such as China that are farther along in the outbreak than the U.S., social distancing and other measures have not been relaxed completely and won’t be for some time—it makes sense to take a gradual approach to returning to “normal.” The size of this resurgence will be a function of our healthcare infrastructure and case tracking capabilities in place to deal with this event.

There is a difficult but important inflection point we’re trying to find: If we reduce isolation and mitigation measures too quickly, we will have a profound impact on morbidity and mortality and risk overwhelming healthcare capacity. If we wait too long, we damage the economy, and put in jeopardy the financial health—and mental health—of our population.

Probabilistic Models Ease Uncertainty

Many in the (re)insurance community leverage probabilistic modeling for pricing, portfolio management, ERM, and other risk management workflows. The life insurance marketplace, too, is gaining momentum for the use of advanced stochastic modeling for pricing, research, risk transfer, and assumption-setting.

Events such as the COVID-19 pandemic highlight the need for insurers, businesses, and governments to understand the possible impact of these catastrophes. The Life and Health team at AIR is modeling high, medium, and low-severity scenarios using our ALERT™ service that can be accessed by ALERT subscribers to understand morbidity, mortality, and other financial impacts.

For More COVID-19 Content, Visit Our Resource Page: COVID-19 Insurance Industry Impacts and Insights