Many of us are already using artificial intelligence (AI) in our daily lives without even noticing; Apple’s Siri, Google Assistant, Microsoft’s Cortana, and Amazon’s Alexa are good examples. The core concept in AI architecture is to mimic the working mechanics of the human brain with advanced algorithms that train themselves from historical data to act rationally when performing tasks.

Advanced algorithms can now crunch massive data sets and understand unstructured data. “Deep learning” is a form of AI that helps machines train themselves to recognize complex and abstract patterns and refine the way they respond to this input, allowing them to recognize written and spoken words and classify visual information.

This technology is spreading into robotics and fueling growth in autonomous systems, such as self-driving cars, and deep-learning algorithms are allowing camera-equipped drones to navigate previously unseen landscapes autonomously. Some real-world insurance-related applications using this technology are already in the pipeline, heralding advances in the collection of high quality data.

Enhancing Data Quality

The accuracy of results obtained from catastrophe models depends on a variety of factors, but the quantity and quality of the data used for developing the model’s components and input into models for analysis (exposure data) have a significant impact.

As well as assessing the major components of properties (structures, walls, roofs, etc.), insurance companies inventory their supporting systems (electrical, plumbing, HVAC, etc.). Information about the surrounding environment that could alter the interaction of the risk with the local hazard is also collected. However, the collection of some of these data is impaired by various access and safety restrictions.

Catastrophe modeling companies commonly employ location-level claims data and post-disaster surveys to construct and revise damage functions and the associated secondary uncertainty around the mean damage. Claims data can also be used to help measure the relative vulnerability between coverages, construction types, and occupancy classes. In addition, these data can also be used to augment the assessment of the local hazard and hazard footprints of historical events, where the resolution of radar and satellite data is not fine enough.

An Eye in the Sky

Many of the challenges faced today by catastrophe modelers, underwriters, and claims adjusters can be improved by using data gathered by AI-managed drones. Drones don’t require takeoff and landing strips, and can hover over properties that may be otherwise inaccessible to capture detailed images and videos of building attributes without risk to humans. Drones with precision cameras can be used, for example, to survey damage in an area impacted by an extreme event for claims adjustment or catastrophe model validation purposes. Drones can also be dispatched to survey damage over a wide area (e.g., crop insurance claims), hail damage to roofs, or other areas that are difficult to view and assess.

In addition to inspection and surveying services, some drones are being developed for the 3D modeling of the major infrastructure damage caused by hurricanes and earthquakes. The object recognition capability of autonomous systems makes drones like these valuable for synthesizing aerial images of risks and their salient attributes both pre- and post-disaster.

The Future Is Here

This is not science fiction; the technology is already being used. Recently, following the devastating Great Ocean Road Bushfire in Victoria, Australia, Insurance Australia Group employed drones to view damage caused by the blaze and fast-track the claims assessment process.

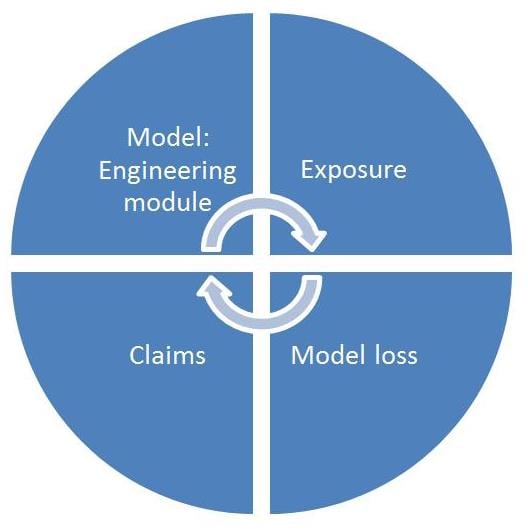

Exposure and claims data quality can be greatly enhanced at the portfolio level with the help of drones. Damage surveys can be performed more efficiently or where a conventional survey would be impossible. For catastrophe model developers and users there is a mutually beneficial interplay between model development, engineering analyses, and exposure and claims data quality. Improving the feedback loop between underwriters, claims adjusters, and model validation (Figure 2) can substantially increase a catastrophe model’s performance in quantifying risk. It seems clear that drones will have an increasingly important role to play in this process, and we are only just beginning to explore it.